Summerhouse Homes for Sale in Crescent Beach / St. Augustine, FL

Gated island condominium community · St. Augustine Beach · ZIP 32080

Gated, amenity-rich condo living on Anastasia Island, with deeded beach access and pools.

Gated, deeded beach accessMultiple pools and tennisTop-rated St. Johns schools

Live Market Pulse

48/100 Momentum

Buyer-Leaning Market (limited data)

A coastal condo market where the building, the view, reserves, and insurance set value as much as the unit; beach access and pools are the draw.

Free · No obligation

Unlock Off-Market Summerhouse

Listings before the portals, true comps, and the renovation and carrying-cost math, before you tour.

Built fromLive realMLS data14 years of closingsLocal renovation analysisUpdated twice daily

LiveMarket PulserealMLS

$432K

Median Price

7.2mo

Supply

55days

Avg DOM

Soft

Seller Leverage

$406/sf

Median $/Sqft

-23%

1-Yr Price Change

0now

Distress

Jon's Current Read

"Summerhouse is a gated, amenity-rich condo play on Anastasia Island, so the read starts with the building, the view, the reserves, and the insurance, not just the unit. Deeded beach access and pools drive demand for primary, second-home, and rental buyers. Confirm the association's health and coverage, then weigh building, floor, and view."

Jon Brooks, founder, Momentum Realty · Updated June 2026

The 60-Second Overview

Summerhouse market snapshot (as of June 13, 2026): the median sale price is about $432K ($406 per sq ft), with homes averaging 55 days on market and 7.2 months of supply, a buyer-leaning market (limited data). Values are down 23% over the past year and up 621% since 2012, based on 5 recent closings in live realMLS data.

Summerhouse is a gated condominium community on Anastasia Island in St. Augustine Beach, St. Johns County, set just off the Atlantic with deeded beach access. Built largely in the 1980s and 1990s, it offers condos in low-rise buildings used as primary residences, second homes, and rentals, with a gated, amenity-rich island setting steps from the sand.

The community pairs multiple pools, tennis and pickleball, a clubhouse and fitness, and deeded beach access with the lock-and-leave convenience of a condo, inside the top-rated St. Johns school district, minutes from St. Augustine Beach and the historic city.

Because this is a condo community, the honest read is the building, the floor, the view, and the association's reserves and structural milestone as much as the unit. Proximity to the beach and the pools and coastal insurance drive value.

Quick Match

Who Summerhouse is best for.

Best for

Buyers who want gated, low-maintenance island living

Second-home, lock-and-leave, and rental buyers

Those who value pools, tennis, and beach access

Top-rated-schools, beach-close buyers

Probably not for

Buyers who want a yard and full cost control

Those who need maximum space per dollar

Anyone wary of condo reserves and coastal insurance

Buyers who dislike shared walls and rules

Market Pulse

How Summerhouse is performing right now

48/100 momentum

Buyer-Leaning Market (limited data)

Seller's marketBalancedBuyer's market

7.2Months of supplytight

22Median days on marketdays

0 : 3Under contract vs for salestrong demand

5Sold in last 12 monthsliquidity

+621%Median price since 2012appreciation

+11%Asking vs recent sold $/sqftroom to negotiate

Tight supply and strong demand favor sellers here. Homes still take about two months to sell, though, and with asking prices running above recent sales per square foot, a prepared buyer has room on anything overpriced. Reading each home against the real comps, not the headline trend, is where the edge is.

Live from realMLS, as of June 13, 2026. Refreshed twice daily. Months of supply, days on market, and the contract-to-listing ratio are computed from current Summerhouse listings and the trailing twelve months of closed sales.

8.6A- score

Momentum intelligence

Momentum buy score

Our proprietary read on how a home in Summerhouse buys, holds, and resells. See the five factors.

Homes For Sale Right Now in Summerhouse

Live MLS inventory for Summerhouse. Every active listing, what is under contract right now, and the last 12 months of closed sales, refreshed twice a day. Closed comps beat an algorithm's guess every time.

No CDD bond means thousands less per year than newer master plans.

Typical CDD community~$2,500/yr

Summerhouse (no CDD)$0/yr

Roughly $25,000 saved over 10 years in carrying cost, before resale.

Illustrative. NE Florida CDD assessments commonly run $1,500-$3,500+/yr and vary by community; verify per property.

Schools

15-Second Take

St. Johns County Public Schools

Verify the zoned schools by address

Magnet and choice options may be available

Confirm current ratings before relying on them

Private and parochial options nearby

Summerhouse is served by St. Johns County Public Schools. Assignment is by address and can change, so confirm the exact zoned elementary, middle, and high schools for any specific home, plus any magnet or choice options. Treat published ratings as a starting point, not the full story.

What is shaping value at Summerhouse: St. Johns County's rapid growth, the strength of the St. Augustine Beach market, set against coastal insurance and Florida's condo reserve rules. Each item is sourced and linked.

Recent Developments in Summerhouse

Development Intelligence

Our read on what is being built around Summerhouse, scored for direction, significance, and how close the effect lands. The full sourced timeline follows below.

Net OutlookBullishCounty growth and fixed island supply point up; the watch item is coastal insurance and condo reserves.

St. Johns County's rapid growth

Ongoing

BullishMajor impact

SignificanceRadius: County

St. Johns added more than 69,000 residents over five years, deepening demand for coastal St. Augustine addresses.

Fixed Anastasia Island supply

Ongoing

BullishMajor impact

SignificanceRadius: Community

Gated, beach-access condos on a built-out barrier island cannot be added to, supporting values.

St. Augustine Beach and tourism demand

Ongoing

BullishNotable impact

SignificanceRadius: Regional

Proximity to the beach and the historic city sustains primary, second-home, and rental demand.

Florida condo reserve and milestone rules

Ongoing

NeutralMajor impact

SignificanceRadius: Community

Stricter reserve and inspection requirements can raise dues or trigger assessments; well-funded buildings are advantaged.

Coastal insurance scrutiny

Ongoing

NeutralNotable impact

SignificanceRadius: Community

Master and flood insurance on the island are real carrying costs and a financing factor.

Direction, significance, and effect-radius ratings are Momentum's proprietary, qualitative read of the sourced items below, not investment advice or a prediction for any specific home.

Development, infrastructure, retail, and school activity affecting Summerhouse, tracked by our team and summarized from public reporting and official sources, with links to the original coverage. Last updated June 2026.

Showing the latest, scroll for all updates ↓

September 2025

Growth

St. Johns County addresses growth and rezoning

County leaders weighed school rezoning amid tens of thousands of new residents over five years. Why it matters: Sustained county growth supports values for scarce island condo communities like Summerhouse. Source

June 2025

Market

St. Augustine Beach remains a strong coastal market

St. Johns County's St. Augustine Beach area continued to draw primary, second-home, and rental demand as the county grew. Why it matters: Beach and historic-city proximity is a durable demand driver for island condos like Summerhouse. Source

Summaries reflect public reporting and official sources linked above as of the dates shown. Project details, timelines, and approvals can change. Commentary on potential market effects is general observation, not investment advice or a prediction for any specific property. For the freshest items across the whole region, see This Week in Northeast Florida.

The Strategy

The Summerhouse buying strategy.

If we were buying in Summerhouse, this is the order of operations we would run, and the one we run for our clients.

1

Read the budget, reserves, SIRS, and any assessments first.

2

Confirm what the dues cover, including pools and beach access, and the all-in monthly.

3

Get wind and flood insurance quotes and confirm the master coverage.

4

Weigh the building, floor, and view of the specific unit.

5

Move on well-run, well-priced beach-close units, which are scarce.

The Quick Decision

Best Buy

A turnkey unit close to the beach and pools in a well-funded building

Biggest Risk

An underfunded coastal association facing reserve assessments

Best Lot

A higher floor or beach-close building with a good view

Smart Timing

Buy once reserves and insurance check out

Deep-Dive Intelligence

The full read, only if you want it.

The takeaway

On mobile, tap any heading below to open it. This is the home by home, lot by lot, club and renovation detail, organized so you can jump straight to what matters to you.

Community Details at a Glance

The Homes

Type

Condominiums in a gated island community

Built

Largely 1980s to 1990s

Size

About 700 to 1,500 sq ft

Status

Established condo resale market

Costs & Fees

HOA

Monthly condo association dues

CDD

None

Taxes

St. Johns County millage; confirm per unit

Amenities

Beach

Deeded Atlantic beach access on Anastasia Island

Pools

Multiple pools, tennis, and pickleball

Community

Gated entry, clubhouse, and fitness

Schools

Top-rated St. Johns County public schools

Location

Area

Anastasia Island, St. Augustine Beach, St. Johns County

Access

A1A and State Road 312 to the mainland

St. Augustine

About 10 to 15 minutes

Beaches

Deeded beach access, steps to the sand

The Homes & Style

Summerhouse is a gated condominium community on Anastasia Island in St. Augustine Beach, set just off the Atlantic with deeded beach access. The units are condominiums in low-rise buildings, largely built from the 1980s and 1990s, ranging from efficient one and two-bedroom plans to larger layouts, many used as primary residences and many as second homes or rentals. The draw is a gated, amenity-rich island setting steps from the beach at a more accessible price than oceanfront.

Because this is a condo community, the practical question is the building, the floor, and the view as much as the unit. For any unit, the association's reserves and the structural milestone matter as much as the finishes, and proximity to the beach, the pools, and a good view drive value.

Living Here

Life at Summerhouse is gated, low-maintenance island living. The community offers multiple pools, tennis and pickleball, a clubhouse and fitness, and deeded beach access, all behind a gate on Anastasia Island, minutes from St. Augustine Beach's shops and restaurants and the historic city across the inlet.

The setting pairs a beach-and-amenity lifestyle with the lock-and-leave convenience of a condo, in the top-rated St. Johns County school district. It is a community for buyers who want the beach, pools, and a gate without the upkeep of a single-family home.

Before You Offer

Read the condo association's finances first: the budget, reserves, the latest SIRS or structural reserve study, and any special assessments. Florida's post-2021 condo rules can raise dues or trigger one-time charges, and a coastal island building deserves extra scrutiny.

Confirm what the dues cover, including the pools, amenities, and any beach-access arrangement, and compute the all-in monthly. Condo dues here are typically higher and cover more.

Get wind and flood insurance quotes and confirm the building's master and flood coverage, since Anastasia Island carries real storm and surge exposure.

Check the unit's building, floor, and view, verify lender acceptance of the association, and confirm any short-term-rental rules if you plan to rent.

Summerhouse vs. Comparable St. Augustine Beach Options

Summerhouse competes with the other condo and beach communities of Anastasia Island and St. Augustine Beach. Against true oceanfront condos, it offers a gated, amenity-rich setting with deeded beach access just off the sand at a more accessible price, while oceanfront units command a premium for the direct water.

Against single-family homes on the island, Summerhouse trades a yard and full control for lock-and-leave convenience, pools, and lower entry pricing. The honest shorthand: pick Summerhouse for gated, amenity-rich, low-maintenance island living near the beach; pick a house for land or an oceanfront unit for the direct water.

Who Summerhouse Fits Best

Summerhouse fits buyers who want gated, amenity-rich, low-maintenance island living with deeded beach access and pools on Anastasia Island, second-home and lock-and-leave buyers who value rental potential and the top-rated schools, and anyone who wants the beach without single-family upkeep.

Summerhouse is a weaker fit for buyers who want a yard and full control of their costs, those who need the most space for the money, or anyone uncomfortable with condo reserves and coastal insurance.

Summerhouse Homes For Sale

What your money buys in Summerhouse.

The takeaway

Three honest price bands. Condition and lot, not the square footage alone, decide where a home lands.

Here are the broad resale bands in Summerhouse today. The right home is the one matched to your budget and the renovation math, so seeing fitting listings early is the edge.

The Entry Unit

$390K to $432K

Smaller one-bedroom and interior units, the lowest-cost entry into gated island condo living.

Lowest entry

The Core Unit

$432K to $460K

Updated two-bedroom units in well-funded buildings, the heart of the market.

Most inventory

The Beach-Close Top

$460K to $460K

Best-position units closest to the beach and pools in the strongest-reserved buildings.

Strongest resale

Approximate 2026 resale bands from third-party listing data and public records, not NEFAR statistics. Confirm pricing for a specific home.

Three realistic price bands. Where a home lands comes down to condition and lot, not square footage alone.

$390K to $432K

The Entry Unit

Smaller one-bedroom and interior units, the lowest-cost entry into gated island condo living.

$432K to $460K

The Core Unit

Updated two-bedroom units in well-funded buildings, the heart of the market.

$460K to $460K

The Beach-Close Top

Best-position units closest to the beach and pools in the strongest-reserved buildings.

Approximate 2026 resale bands from third-party listing data and public records, not NEFAR statistics. Confirm pricing for a specific home.

Operator Intelligence

Renovation & Resale Intelligence

The factors that actually move value in Summerhouse, condition, lot, and the renovation math, read from current listings and recent sales.

15-Second Take

Renovation math decides the deal

Better lots and views resell strongest

Roof and HVAC age drive the insurance quote

Interior lots are where buyers overpay

Proprietary Data

The renovation premium.

Updated homes ask about 33% more per square foot than original-condition homes, and they tend to sell faster. In an all-resale market, condition is the single biggest swing in value, which is why reading the renovation math is the whole game.

Asking price per square foot

Renovated$505

Original$381

Median days on market

Renovated72

Original22

From current Summerhouse listings (renovated 2, original 1); condition inferred from listing descriptions, asking not closed figures. The exact number depends on a specific home's updates, lot, and view, which is the read we do before you offer.

Operator Note

The trap here is a beautifully staged original-condition home. Staging is cheap; a roof, HVAC, and a full modernization are not. We price the real renovation before you fall for the listing photos, because in an all-resale market that number is the difference between a deal and the most expensive house on the street.

Unit Value

The unit premium.

In a condo the value the market gives back at resale is set by the unit, not a lot: the floor, the view line (direct versus partial), and the exposure. The interior can be renovated, but the floor and view cannot, so higher floors and better views hold their value better. How much more they command varies by building, line, and condition, which is why we read it unit by unit against real comparable sales rather than a single headline figure.

Operator Note

Most buyers overpay on interior lots in the back half of the community. A sharp renovation can distract you, but the weaker resale position follows the lot, not the finishes. We read the homesite before the kitchen.

Resale Strength Scorecard

How well Summerhouse holds value.

Our read on the factors that protect resale here, and the one to manage.

Gated island, deeded beach accessStrong

Pools, tennis, and amenitiesStrong

Top St. Johns schools and beach proximityPositive

Fixed island supplyPositive

Coastal insurance and condo reservesBudget it

Momentum analysis based on the community's structure, location, lot scarcity, and housing stock. Not a guarantee of future value.

Operator Note

The strongest value pocket is usually a renovated home on a good lot priced just under the next tier up. Buyers chasing the single biggest house often pay top prices for what is really a renovation project.

5 Mistakes Buyers Make in Summerhouse

15-Second Take

Calling the listing agent (who works for the seller)

Misjudging the renovation budget

Overpaying for an interior lot

Underbudgeting the carrying costs

Skipping the roof, HVAC, and systems check

The same five mistakes cost buyers the most in any market. Every one is avoidable with the right preparation before you tour.

1

Calling the listing agent

The agent on the sign works for the seller. In a market where condition swings price by hundreds of thousands, negotiating against that agent with no one in your corner is the costliest move of all.

2

Misjudging the renovation math

A dated home looks like a deal until you price the roof, HVAC, pool, and full modernization honestly. Underbudget the reno and the bargain becomes the expensive house.

3

Overpaying for an interior lot

A premium homesite (water, preserve, or a preferred position) carries a real, durable premium. Pay a top price for an interior lot and you are buying the weakest version of the value.

4

Underbudgeting the carrying costs

Two similar homes can cost very differently to own once the HOA, any CDD, insurance, and upkeep are priced in. Buyers who do not run the full monthly carrying cost misread the real number.

5

Skipping the systems check

An older home means older systems unless updated. Roof age, HVAC age, pool equipment, and prior renovations drive both price and insurability, and a thorough inspection matters more here than in a new build.

“

On the island you buy the building and its insurance as much as the unit. Reserves, coverage, and the view decide the number.

Jon Brooks · Founder, Momentum Realty

Momentum Intelligence

Momentum Buy Score.

Our proprietary 0 to 10 read across the five factors that decide how a home here buys, holds, and resells.

8.0A- · Buy Score

Resale Strength8.0/10

Renovation Risk7.4/10

Location Efficiency8.8/10

Long-Term Defensibility8.2/10

Carrying Cost Advantage6.0/10

Momentum Intelligence Scores are our proprietary, qualitative assessment based on the analysis on this page, on a 0 to 10 scale. They are a framework for comparing communities, not a guarantee of future value or advice on a specific home.

Momentum Housing Intelligence

Why our read on Summerhouse is different.

Most pages on this community are an automated estimate wrapped in stock copy. This one is built from the live realMLS feed, fourteen years of closed sales, and a renovation-by-renovation read of what actually moves value here, lot by lot. No Zestimate, no guesswork.

Live realMLS feed14 years of closed salesRenovation-premium analysisLot-by-lot, no automated estimates

Jon Brooks, founder of Momentum Realty. A housing economist with a background in real estate investment banking at Deutsche Bank and consulting at Ernst & Young, who has built and analyzed Northeast Florida real estate from the ground up.

Where the value actually sits. Each home is shaded by its price per square foot (a value read, not just a price) and ringed by lot type, so you can see at a glance which pockets carry a real, durable premium and where a renovation play makes sense.

Value ($/sqft)

$261 value$401 premium

Fill = price per square foot; ring = by realized $/sqft per unit. Sold homes are shown by realized $/sqft (lot type not always recorded). Asking and recent-sold figures from realMLS; for orientation, not an appraisal.

15-Second Take

Beach and pool proximity drive value most

The building's reserves matter as much as the unit

Higher floors and good views carry a premium

The unit's finishes can change; the building cannot

Read reserves and insurance before the finishes

In an island condo community your money buys a share of the building, so the association's reserves, the structural milestone, and the master and flood insurance are the durable part of the value. Within that, proximity to the beach and pools, the floor, and the view drive day-to-day living and resale. Read the reserves and the insurance first, then weigh the unit.

The 15-Second Verdict

Summerhouse in 15 seconds.

Best forbuyers who want gated, amenity-rich island condo living near the beach.

Biggest advantageDeeded beach access, pools, and tennis behind a gate in top schools.

Biggest riskCoastal insurance and condo reserves under Florida's newer rules.

Sweet spotA turnkey beach-close unit in a well-funded building.

Avoid ifyou want a yard and full control of your costs.

HOA, CDD & Fees

15-Second Take

Monthly condo dues fund pools and amenities

Review reserves and the structural study

Confirm beach access and any assessments

Dues often include master insurance

Budget coastal insurance into the carrying cost

Summerhouse carries monthly condominium association dues funding the gate, multiple pools, tennis and pickleball, the clubhouse and fitness, grounds, building exteriors, and master insurance, plus deeded beach access. Under Florida's newer condo laws, review the budget, reserves, the structural study, and any assessments, and add coastal insurance to the carrying cost.

Dues typically cover exterior and roof maintenance, grounds, the gate, the pools and amenities, master insurance, and the beach-access arrangement, leaving the owner responsible for the interior and contents.

Community amenities run through the association: a gated entry, multiple pools, tennis and pickleball, a clubhouse, fitness, and deeded beach access, rather than a private country club.

Run Your Numbers

Tools for a Summerhouse buy.

Free calculators to pressure-test the real cost before you tour.

Selling here is won on condition and view, not the Zestimate. The right number comes from closed comps matched to your renovation level and lot.

Selling in Summerhouse

Price it to the building's health, the beach proximity, and the view, not square footage alone.

If you are thinking about selling in Summerhouse, the right list price comes from recent comparable unit sales in this community, matched to your building, floor, beach proximity, and the association's standing, not an automated estimate.

Momentum listings (YTD)

97.98%

Sold-to-list ratio across the Jacksonville metro for our agents, sellers keeping more of their price.

Market average (YTD)

96.73%

The broader metro average sold-to-list ratio over the same period.

Momentum days on market

64 days

Median days on market for our listings, faster sales mean less carrying cost and stronger leverage.

Market days on market

72 days

The broader metro median over the same period.

Sold-to-list and days-on-market figures reflect Momentum Realty listings versus the Jacksonville metro average, year to date. Your home's result depends on pricing, condition, lot, view, and preparation.

In Summerhouse, condition and view decide your number

Because buyers here are weighing your home against renovated comps and cross-shopping Marsh Creek, a home priced to the community average instead of its true condition and view either leaves money on the table or sits. A renovated kitchen, newer roof and HVAC, and a golf or lake view all deserve to show up in your price, and a buyer pool reading renovation math needs to be shown why your home is worth it. We build that case with real comps and a pricing strategy for the current market.

What is your Summerhouse home worth?

Get a no-obligation home value based on real comparable sales in Summerhouse matched to your condition, lot, and view, not an automated guess. Tell us about your home and we will personally prepare your numbers and a pricing strategy. No obligation, no spam.

Price History: What Homes Here Have Actually Sold For

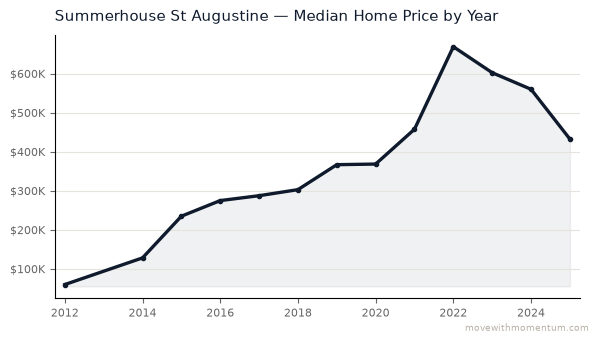

Median sale prices in Summerhouse year by year since 2012, from closed MLS sales. A long track record beats a single estimate, showing what this community has really done through rate cycles rather than what a model predicts.

How much local inventory is already under contract

19% of homes for sale in ZIP 32080 are already under contract (under contract ÷ under contract + active listings) — a read on how much of the available inventory buyers have already claimed. Source: MLS data (2026-06-24).

Summerhouse Market Scorecard

Balanced

Summerhouse is currently a balanced. About 4.8 months of supply, a median asking price of $537,000, and homes go under contract in about 84 days.

4.8

Months supply

$537,000

Median list

$432,500

Median sold

$505

Per sqft

84

Days on mkt

2/1/5

Active/Pend/Sold

Typical home value in the 32080 ZIP is $537,142, about 18.6% above the Florida norm (Zillow Home Value Index).

Live data: realMLS, refreshed twice daily. Typical value: Zillow Research. Market metrics only; these describe homes for sale and recent sales, not residents.

Frequently Asked Questions

Can I really do short-term rentals, and is there a minimum stay?

Yes, short-term renting is the established culture here, with nightly and weekly stays running through the on-site program and the major platforms. The association publishes rules and regulations governing guests, occupancy, parking, and pets, and rental policies live in the condominium documents, which can be amended, so we confirm the current minimum-stay rules, registration requirements, and any program obligations in writing before you buy. If your underwriting depends on a specific rental model, that confirmation is non-negotiable.

Do I have to use the on-site rental office?

No. Summerhouse Rentals Inc. is the association-affiliated on-site program, and many owners use it for its front desk, housekeeping, and decades of repeat guests, but owners can also hire outside vacation-rental managers or self-manage on Airbnb and Vrbo. Each path has a different commission and workload profile; we help clients compare SRI's current terms against third-party managers before closing so the income plan is real on day one.

What is the pet policy?

Owners may have pets, with breed and number restrictions in the association's rules; rental guests face tighter limits that vary by unit and program. If pets matter to your own use or to your rental strategy, pull the current rules and the unit's rental-program pet status rather than relying on a listing remark, because pet-friendly units book differently than pet-free ones.

What is it like in the off-season?

Quiet, and that is the point. Summer weekends fill the pools and the walkovers; by late fall the property belongs to snowbirds, long-weekenders, and the full-time handful, and Crescent Beach itself empties to locals walking dogs at low tide. Owners who want energy year-round tend to prefer St. Augustine Beach; owners who want January on a near-empty beach ten minutes from a 450-year-old city consider this the best season of all.

Where is Summerhouse located?

Summerhouse Beach & Racquet Club is at 8550 A1A South on the southern end of Anastasia Island at Crescent Beach, in unincorporated St. Johns County, Florida (ZIP 32080), beside the state park land that wraps Matanzas Inlet and Fort Matanzas National Monument. Downtown St. Augustine is roughly 10 miles north, about a 15-20 minute drive.

How many units does Summerhouse have, and when was it built?

256 condominium units in two-story buildings across four phases on roughly 25 oceanfront acres. The community was established in 1982 and built out through the four phases; there are no elevators anywhere on the property.

Is Summerhouse gated?

Yes. Summerhouse is a gated community with the office staffed seven days a week and full-time maintenance on site, which is part of why it functions so well as a managed vacation-rental property.

What unit types are available?

First-floor single-level flats and second-floor townhouse-style condos with interior stairs, mostly two-bedroom, two- or two-and-a-half-bath plans of roughly 1,064 to 1,280 square feet, plus a smaller number of three-bedroom plans. Position, not floor plan, drives most of the price spread.

What are the condo fees, and what do they include?

Recent listings have reported association fees of roughly $645-$682 per month with unusually broad inclusions: water, sewer, trash, cable, the master insurance, exterior and grounds maintenance, pest control, management, security, and all four heated pools. There is no CDD. Fees move with insurance renewals, so confirm the current budget for any specific unit before you offer.

Has Summerhouse had special assessments?

Owners have reported a one-time special assessment of roughly $10,000 per unit in recent years to fund balcony repairs, exterior paint, and roof replacement, the kind of capital program every 1980s coastal complex eventually runs. Verify the assessment status on any specific unit and read the reserve study and meeting minutes for what comes next; we pull that file on every purchase we represent.

Do Florida's milestone inspection and SIRS laws apply to Summerhouse?

Florida's post-Surfside milestone and SIRS regime is written around buildings three stories and higher, and Summerhouse's two-story construction generally sits outside the strictest of those mandates, which is a real cost advantage versus the mid-rise towers. It is not a free pass: 40-year-old roofs, balconies, and walkovers in salt air still demand a funded reserve plan, and the association's budget and engineering history tell you how well that is going. Confirm the current compliance posture in the documents.

Are short-term rentals allowed at Summerhouse?

Yes, and they are the established culture: nightly and weekly vacation rentals run through the on-site program and the major platforms, which is exactly the flexibility most owner-occupied complexes up the island have voted away. Rules on minimum stays, guest registration, parking, and pets live in the association's documents and can change, so confirm the current rental rules in writing before you buy if your underwriting depends on them.

How does the on-site rental program work?

The association's board formed Summerhouse Rentals Inc. (SRI) in 1998 as its own licensed brokerage to run the on-site rental program, with a front desk staffed seven days a week, housekeeping, maintenance, and an owner portal. Owners can use SRI, hire an outside vacation-rental manager, or self-manage on Airbnb and Vrbo; we help clients compare SRI's current commission and program terms against third-party options before closing.

What can a Summerhouse condo earn as a vacation rental?

Published nightly rates on the major platforms have averaged roughly $200-$250 for two-bedroom units, higher in peak summer, and well-run units are commonly discussed in the $30,000-$50,000 gross-per-year neighborhood depending on position, calendar management, and reviews. Treat every specific claim as unverified until you see trailing-12-month statements, and remember that management, cleaning, dues, taxes, insurance, and furnishings commonly consume half or more of gross before debt service.

What are recent Summerhouse prices?

Current asks have run from $499,000 (interior/road-side positions) to $769,000 (direct oceanfront), almost all on ~1,064 sq ft two-bedroom plans, with 2024 oceanfront closings at $685,000-$745,000 and a late-2025 closing at $440,000 off a $498,000 ask after 167 days on market. The market softened meaningfully through 2025, days on market run long, and closings under ask are the norm, which is real leverage for prepared buyers.

What amenities do owners and guests get?

Four heated pools (one per phase, all shared), four private dune walkovers, six tennis courts, pickleball, four racquetball courts, basketball, shuffleboard, horseshoes, playgrounds, a fitness room, a business center, covered pavilions, grills, and a boat and RV storage yard with a wash-down area. The office is staffed seven days a week and maintenance is on site.

What is Crescent Beach like compared to St. Augustine Beach?

Crescent Beach is the quiet end of the island: wide sand, a designated driving beach north of the property (county ramp at Cubbedge Road), and a vehicle-free stretch south of Summerhouse running toward Fort Matanzas and the last natural inlet on Florida's east coast. St. Augustine Beach, 10-15 minutes north, has the pier, the restaurant rows, and the crowds. Summerhouse buyers and rental guests generally choose this end specifically for the quiet.

What about flood zones, erosion, and insurance?

This is a barrier-island oceanfront property, and the 32080 ZIP carries meaningful flood-risk flags in third-party data. The master wind policy lives inside the association dues and moves with every renewal; your own HO-6 walls-in policy with appropriate wind and flood treatment is on top. Pull the FEMA zone for the parcel, quote real insurance on the specific unit, and read the association's storm-repair history before you write.

What schools serve Summerhouse?

St. Johns County schools, typically W. Douglas Hartley Elementary (strong GreatSchools rating), Gamble Rogers Middle, and Pedro Menendez High. Most buyers here are investors and second-home owners, but the A-rated county district quietly supports resale. Assignment is by address and changes periodically, so confirm zoning for a specific unit with the district.

Do I need my own agent to buy at Summerhouse?

Yes. The listing agent works for the seller. Your own agent verifies the fee, insurance, and assessment file, demands real trailing-12 rental statements instead of projections, comps the position rather than the floor plan, and negotiates the soft-market leverage for you. Momentum Realty will connect you with a Summerhouse specialist; call (904) 351-6461 or use the form on this page.

The Verdict

Should you buy in Summerhouse?

An honest fit check. We will tell you when it is not your community.

You want gated, amenity-rich island condo livingExcellent fit

You value deeded beach access and poolsExcellent fit

You want a second-home, lock-and-leave, or rentalExcellent fit

You will budget coastal insurance and reservesExcellent fit

You want a yard and full cost controlProbably not

You need maximum space per dollarProbably not

You are wary of condo reserves and coastal insuranceProbably not

You dislike shared walls and rulesProbably not

Get the inside read on Summerhouse

Whether you are buying a renovation project, comparing the lots and views, weighing the carrying costs, or selling your Summerhouse home, tell us what you need. Every inquiry comes straight to us. We represent you, not the seller, and what your agent is paid is negotiable and set in a written buyer agreement up front. No obligation, no spam, no high-pressure follow-up.

You are all set.

A Momentum Realty Summerhouse specialist will reach out personally, usually the same day.

Photography on this page is sourced from active and recently sold MLS listings in this community and remains the property of the listing brokerage and/or photographer. Source: Data provided by realMLS.

Thinking about hiring an agent here? How to find the best real estate agent in Summerhouse — what to look for, questions to ask, and your local expert.Median sale price in Summerhouse St Augustine, Florida by year (2012 to 2025). Source: Momentum Realty.

Get a real cash offer on your Summerhouse home in 24 hours and close in as little as 7 days, as-is. Because Momentum is a licensed RealTrends-500 brokerage, we'll also show you what listing would net — so you choose with both numbers.

Buying or researching St. Johns County? See the full St. Johns County real estate market report — prices, inventory, schools, taxes, and every St. Johns County neighborhood.

Own a home here?

You just read the data. Now see what your home is worth.

The numbers on this page move markets in the aggregate. The number that matters to you is what a buyer pays for your address. Momentum sells for 1.25% above the RealMLS member average and 8 days faster, and we’ll price yours against live your area comps.